Many Indians buy insurance because a friend, bank executive, or relative suggested it. But later, they realize they never truly understood what they purchased. One of the biggest confusions people still have in India is the difference between term insurance and life insurance.

Some people think both are the same. Others believe term insurance is a waste because there is no maturity benefit. On the other hand, many avoid traditional life insurance plans because the returns are low.

The truth is — both serve different financial purposes.

If you are planning your family’s financial security, taking a home loan, raising children, or thinking about long-term savings, understanding this difference is extremely important in 2026.

In this guide, we will explain everything in simple language with Indian examples, pricing, benefits, drawbacks, and expert tips.

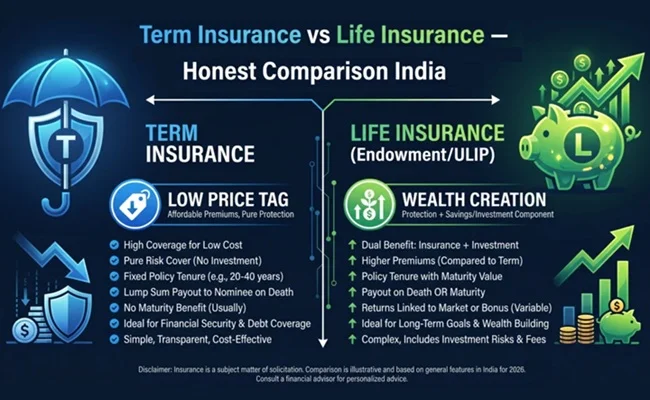

What is Term Insurance?

Term insurance is a pure protection plan. It gives financial security to your family if something happens to you during the policy period.

If the insured person dies during the term, the nominee receives the sum assured. If the policyholder survives the term, no maturity amount is paid in a standard term plan.

Simple Example

Rahul, age 30, buys a ₹1 crore term insurance plan for 30 years.

- Annual premium: Around ₹12,000–₹18,000

- If Rahul dies during the policy period, his family gets ₹1 crore.

- If he survives 30 years, there is usually no payout.

Term insurance is designed mainly for income protection.

What is Life Insurance?

In India, people often use the term “life insurance” for traditional insurance plans that combine insurance plus savings or investment.

These plans may include:

- Endowment plans

- Money-back policies

- Whole life insurance

- ULIPs (Unit Linked Insurance Plans)

Such policies provide:

- Life cover

- Maturity benefit

- Bonus or investment returns

Example

Amit buys a traditional life insurance policy with:

- ₹10 lakh cover

- 20-year duration

- Annual premium of ₹55,000

If Amit survives the term, he receives maturity benefits plus bonuses.

If he dies during the policy period, the nominee gets the insured amount.

Difference Between Term Insurance and Life Insurance

Comparison Table

| Feature | Term Insurance | Traditional Life Insurance |

| Purpose | Financial protection | Protection + savings |

| Premium | Very low | Higher |

| Maturity Benefit | Usually no | Yes |

| Coverage Amount | Very high | Lower compared to premium |

| Investment Component | No | Yes |

| Returns | None | Moderate |

| Ideal For | Family protection | Conservative savers |

| Tax Benefits | Yes | Yes |

| Risk Cover | Excellent | Limited |

| Flexibility | High | Medium |

Key Features of Term Insurance

Benefits of Term Insurance

- Affordable premiums

- High life cover at low cost

- Ideal for breadwinners

- Financial protection for family

- Useful for home loan protection

- Tax benefits under Section 80C and 10(10D)

- Riders available for critical illness and accidental death

Key Features of Traditional Life Insurance

Benefits of Life Insurance Plans

- Insurance plus savings

- Maturity payout available

- Lower financial risk

- Suitable for disciplined savings

- Some plans provide guaranteed returns

- Long-term wealth accumulation

Who Should Choose Term Insurance?

Term insurance is suitable for:

- Salaried employees

- Young parents

- Home loan borrowers

- Business owners

- People with financial dependents

- Individuals wanting high coverage at low cost

Ideal Age to Buy

The best time to buy term insurance in India is between 25 and 35 years because premiums are lower.

Who Should Choose Life Insurance Plans?

Traditional life insurance may suit:

- Conservative investors

- People uncomfortable with market risk

- Individuals seeking forced savings

- Senior citizens wanting stable returns

- Parents planning long-term savings

Step-by-Step Guide to Choose the Right Insurance

Step 1: Identify Your Goal

Ask yourself:

- Do you only need family protection?

- Or do you also want savings and maturity benefits?

Step 2: Calculate Required Coverage

Experts in India usually recommend:

- 10 to 15 times your annual income

Example:

If your annual income is ₹10 lakh:

- Recommended term cover = ₹1 crore to ₹1.5 crore

Step 3: Compare Premiums Online

Use platforms like:

- Policybazaar

- Turtlemint

- Ditto Insurance

- InsuranceDekho

Compare:

- Claim settlement ratio

- Premium amount

- Riders

- Customer reviews

Step 4: Check Claim Settlement Ratio

Choose insurers with:

- 95%+ claim settlement ratio

- Good customer service

- Strong financial reputation

Step 5: Read Policy Terms Carefully

Never ignore:

- Waiting periods

- Exclusions

- Claim conditions

- Premium payment rules

Eligibility Criteria in India

For Term Insurance

| Criteria | Requirement |

| Minimum Age | 18 years |

| Maximum Entry Age | Usually 60–65 years |

| Citizenship | Indian resident/NRI |

| Income Proof | Required for high coverage |

For Life Insurance Plans

Eligibility varies by policy type, but most plans require:

- Valid KYC

- Age proof

- Income proof

- Medical tests (in some cases)

Documents Required

Common Documents Needed

- Aadhaar Card

- PAN Card

- Address proof

- Income proof

- Passport-size photograph

- Bank statements

- Medical reports (if required)

Pricing Comparison in India (2026)

Approximate Premium Comparison

| Age | Term Insurance ₹1 Crore | Traditional Life Insurance ₹10 Lakh |

| 25 years | ₹9,000–₹12,000/year | ₹40,000–₹70,000/year |

| 30 years | ₹12,000–₹18,000/year | ₹50,000–₹80,000/year |

| 40 years | ₹25,000–₹40,000/year | ₹80,000+ |

Premiums vary depending on health, smoking habits, and insurer.

Pros and Cons

Pros of Term Insurance

Advantages

- Cheap premiums

- High coverage

- Simple structure

- Best for financial security

Disadvantages

- No maturity amount

- No savings component

Pros of Traditional Life Insurance

Advantages

- Maturity benefits

- Savings discipline

- Guaranteed returns in some plans

Disadvantages

- Lower insurance coverage

- Expensive premiums

- Returns may not beat inflation

Common Mistakes Indians Make

- Mixing Insurance with Investment

Insurance should primarily provide protection. Investment goals should usually be handled separately.

- Buying Low Coverage

A ₹5–10 lakh policy is often insufficient for modern family expenses in metro cities.

- Delaying Purchase

Premiums rise with age and medical conditions.

- Hiding Medical Information

Incorrect declarations can lead to claim rejection.

- Choosing Based Only on Premium

Cheapest plans are not always the best.

Best Expert Tips for 2026

Buy Term Insurance Early

Buying at age 25 can save lakhs in premiums over time.

Separate Insurance and Investments

Many financial planners in India now recommend:

- Term insurance for protection

- SIPs/mutual funds for wealth creation

Add Useful Riders

Consider:

- Critical illness rider

- Waiver of premium rider

- Accidental death benefit

Increase Cover After Major Life Events

Review insurance after:

- Marriage

- Childbirth

- Home loan

- Salary increase

Latest Insurance Trends in India (2026)

Rise of Digital Insurance

Most Indians now purchase insurance online because:

- Lower premiums

- Faster approval

- Easy comparison

AI-Based Policy Issuance

Many insurers now offer:

- Instant policy approvals

- Video KYC

- Faster claim processing

Customizable Plans Becoming Popular

Users can now customize:

- Coverage amount

- Riders

- Premium payment options

Women-Specific Insurance Benefits

Some insurers offer:

- Lower premiums for women

- Pregnancy-related benefits

- Wellness rewards

Best Term Insurance Options in India (2026)

Popular Choices

| Insurance Company | Popular Plan |

| LIC | LIC Tech Term |

| HDFC Life | Click 2 Protect Super |

| ICICI Prudential | iProtect Smart |

| Max Life | Smart Secure Plus |

| Tata AIA | Sampoorna Raksha |

| SBI Life | eShield Next |

Best Traditional Life Insurance Options

| Company | Popular Plan |

| LIC | Jeevan Anand |

| HDFC Life | Sanchay Plus |

| ICICI Prudential | Guaranteed Income Plan |

| Bajaj Allianz | POS Goal Suraksha |

| SBI Life | Smart Wealth Builder |

FAQs

Q: Is term insurance better than life insurance?

A: Term insurance is better for pure financial protection because it offers higher coverage at lower cost.

Q: Why is term insurance cheaper?

A: Because it only provides risk cover and does not include savings or investment components.

Q: Can I get maturity benefits in term insurance?

A: Yes, some plans offer “Return of Premium” options, but premiums are higher.

Q: How much term insurance cover should I buy?

A: Most experts recommend coverage worth 10–15 times your annual income.

Q: Is LIC term insurance good?

A: LIC Tech Term is considered reliable, especially for people preferring government-backed insurers.

Q: Can salaried employees buy term insurance online?

A: Yes, most insurers offer fully digital purchase processes in India.

Q: Which is better for investment: ULIP or term insurance?

A: Term insurance is for protection, while ULIPs are investment-linked products. They serve different purposes.

Conclusion

Choosing between term insurance and life insurance depends on your financial goals.

If your priority is protecting your family at an affordable cost, term insurance is usually the smarter option. It gives large coverage without putting pressure on your monthly budget.

If you want a combination of insurance and savings with guaranteed payouts, traditional life insurance plans may suit you better.

For most middle-class Indian families in 2026, financial experts recommend:

- Buy adequate term insurance first

- Build investments separately through SIPs, mutual funds, PPF, or other instruments

The key is not just buying insurance — it is buying the right insurance for your life stage and responsibilities.